I’m Underwater on $SNAP and I’m Still Bullish. Here’s Why.

A bullish case for Snap Inc., anecdotal evidence, a pricing model, and a stock down 30%.

My boys don’t text people. Not really. If you send them an SMS, you might as well have sent a fax.

They Snap.

Their friends Snap. Their social operating system runs through Snapchat, and it has for years. I’ve watched it up close long enough to know this isn’t a phase. It’s a habit. And habits in 14-year-olds have a way of becoming infrastructure.

So when $SNAP started showing up in my options screening, I didn’t need a Wall Street thesis to get interested. I had two teenagers and a lot of anecdotal evidence sitting in my house.

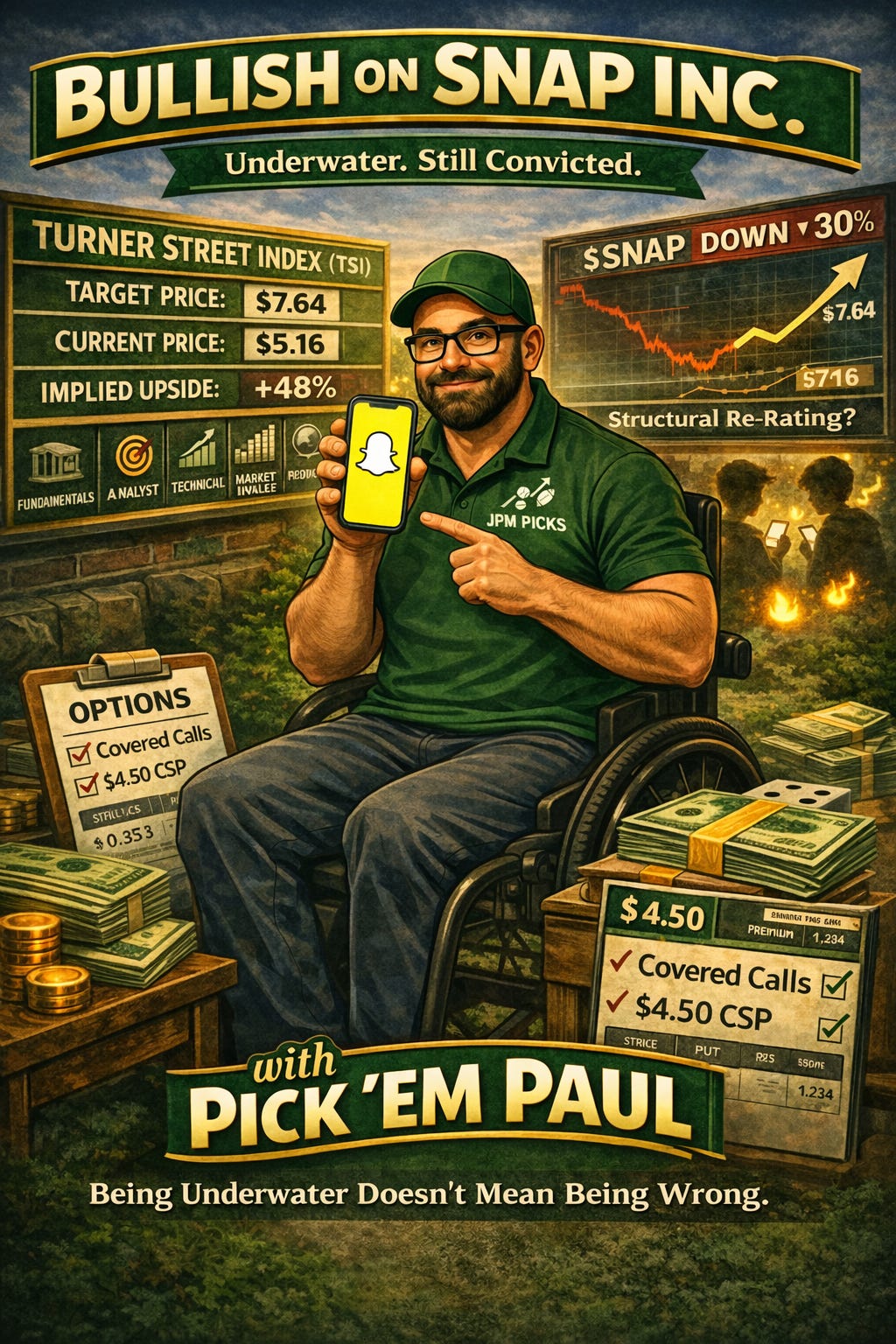

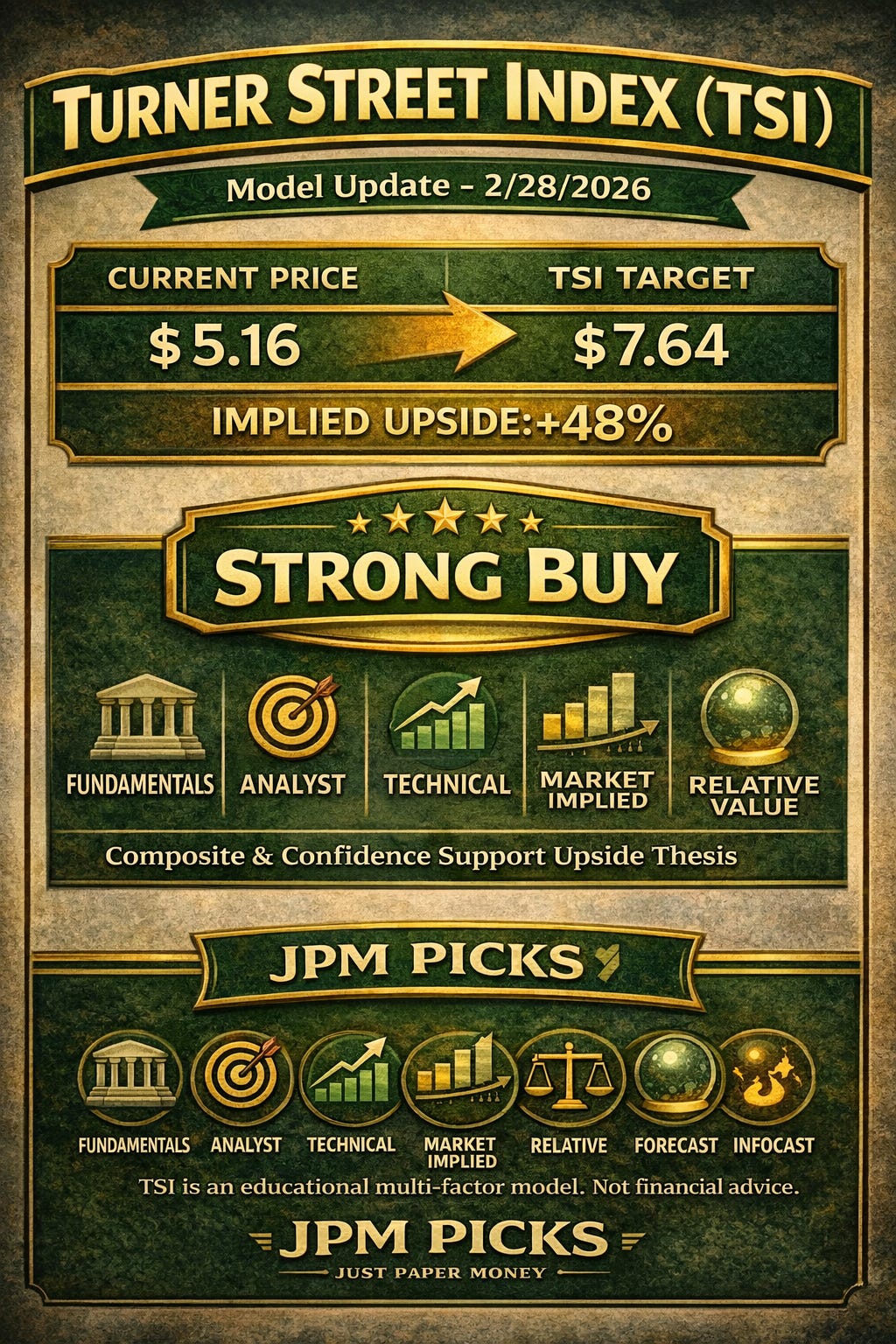

I ran it through my model, which I call the Turner Street Index (or TSI). I got a target price of $7.64.

The stock is currently trading around $5.16. It’s down over 30% in the past month.

I own shares. I’m underwater. And I’m still bullish.

Here’s the honest version of why. Bear case included.

First: What Is the Turner Street Index?

Before I get into the $SNAP case, let me explain where that $7.64 number comes from.

The Turner Street Index (TSI) is a multi-factor stock evaluation model I built to give myself a structured, repeatable way to evaluate equities. It’s not a crystal ball. It’s a framework.

The TSI scores a stock across six pillars, each rated 0 to 10:

• Fundamentals 🏦: P/E vs peers, PEG ratio, dividend yield, ROE

• Analyst 🎯: where analysts have price targets relative to current price

• Technical 📈: moving average alignment and RSI

• Market Implied 📊: options market signals like put/call ratio and implied volatility

• Relative Value ⚖️: how the stock is valued versus its peers

• Forecast 🔮: probability-weighted bull/base/bear scenario expected value

Those six scores get blended into a Composite Score (0-10), a Consistency Score (how much the pillars agree with each other), and a Confidence Score (0-100%) that combines upside, composite, and consistency into a single conviction number.

The output is a target price and a rating: Sell, Hold, Buy, or Strong Buy.

After re-running $SNAP through the TSI with post-earnings data: JPM Picks Target Price: $7.64. Current Price: $5.16. Implied Upside: +48%.

A note on process, and why this matters.

My original TSI target on $SNAP was $10.04. That number was built months ago and never updated when new earnings came in. That stale target is exactly why I was comfortable selling cash-secured puts closer to fair value than I realized at the time. The gap between $10.04 and $7.64 tells you everything about what one or two earnings cycles can do to a stocks outlook.

Lesson learned, and worth sharing: update your model when earnings drop. A stale target price is worse than no target price because it gives you false confidence. I’m writing that down so you don’t make the same mistake.

The TSI is an educational framework. Scores reflect relative rankings, not guaranteed price paths. Not financial advice.

The Bear Case. And It’s Real.

Let’s not skip past this. The market didn’t panic for no reason. If you’re thinking about $SNAP right now, you need to understand what spooked everyone after Q4 2025 earnings.

• North American DAUs dropped hard. Daily active users in North America fell by 4 million in a single quarter, from 98 million to 94 million. That’s Snap’s most monetizable user base, and it shrank.

• Q1 2026 guidance missed. Snap guided $1.50B-$1.53B in Q1 revenue. Wall Street wanted $1.55B. Not catastrophic, but enough to confirm the bear narrative.

• The CTO sold shares. $SNAP’s Chief Technology officer, Robert C. Murphy sold 2 million shares near all-time lows. Worth noting, it was under a pre-arranged trading plan, not a spontaneous sell. Still, the timing doesn’t help sentiment.

• Regulatory risk is real. Age verification laws are already costing users in Australia. More legislation is working through the courts in the U.S. If Snap’s core demographic gets legislated off the platform in key markets, that’s an existential problem, not a quarterly blip.

I’m not going to tell you those concerns are wrong. They’re legitimate. The market isn’t stupid.

But I don’t think the market is entirely right either.

The Bull Case. What Didn’t Make the Headlines.

Here’s what got buried under the DAU noise:

• Revenue beat. Q4 revenue came in at $1.72 billion, up 10% year-over-year, ahead of estimates.

• They actually made money. Net income was $45 million, compared to $9 million a year ago. This is a company that bled red ink for years. Profitability is new, and it’s real.

• EBITDA expanded. Adjusted EBITDA hit $358 million, up from $276 million the prior year. Margins are moving in the right direction.

• Snapchat+ is growing fast. Subscribers hit 24 million, up 71% year-over-year. That’s recurring subscription revenue, not purely ad-dependent. It matters more than people think.

• $2.9 billion in cash. They’re not going anywhere. And they announced a $500 million stock buyback. At $5 a share, that buyback hits differently than it does at $11.

• 946 million monthly active users. Approaching 1 billion. The engagement isn’t gone. It’s the daily monetizable users in North America that are the problem. That’s a real problem, but it’s a different problem than nobody uses Snapchat anymore.

And here’s the part the model can’t fully capture: my kids still can’t put it down.

Every generation gets one or two apps that become genuinely load-bearing in their social lives. For Gen Z and the cohort behind them, Snapchat is one of those apps. You don’t just delete load-bearing infrastructure because the stock price is struggling.

The Trade. Full Transparency.

I own shares of $SNAP. I’m underwater on the position. I’m not going to get into the exact numbers, but I’ll tell you this: I entered with conviction, the stock has moved against me, and I haven’t flinched.

Being underwater doesn’t mean being wrong. It means being early, or being wrong, and you don’t always know which one it is until more time passes.

What I’m not doing is letting a bad month talk me out of a thesis I built before the noise started.

What I’m planning next: I’m going to start selling covered calls on my shares to grind down my cost basis while I wait. Premium doesn’t fix everything, but it’s better than just watching a red position and doing nothing.

If you’re not familiar with how covered calls work as a cost basis tool, that’s exactly what the Options 101 post covers. The short version: you collect premium on shares you already own, and that premium slowly chips away at what you paid.

Would I Sell a Cash-Secured Put on $SNAP Right Now?

This is the question I run through my checklist every time before I sell any put. Let’s walk through it for $SNAP at current prices.

• ✅ Is this a stock I’d be comfortable owning long term? Yes. I already own it and I’m not flinching.

• ✅ Do I understand the business? Camera company. Messaging app with near-total penetration in the 13-25 demographic. Pivoting toward subscriptions and AR. One sentence: Snapchat owns the social layer of Gen Z’s daily life and is trying to monetize it without killing it.

• ✅ Is the options market liquid enough? Yes. Active options chain with reasonable spreads.

• ⚠️ Where are we in the chart? Down 30%+ in a month off earnings. That’s not a normal dip. That’s a structural re-rating. Catching a falling knife is a real risk. I’d want to see the stock stabilize before pressing harder.

• ⚠️ Is there more bad news coming? Potentially. Regulatory risk isn’t priced out. Q1 guidance was soft. The next earnings report will matter a lot.

My honest answer: I’m not adding aggressively at $5. But if I didn’t already own shares and my TSI still says $7.64, I’m looking at the $4.50 strike cash-secured put, far enough out of the money to give the stock room to breathe, with enough premium to make the wait worthwhile.

What Would Break the Thesis

The thesis breaks if:

• North American DAUs keep falling for 2-3 more quarters without finding a floor

• The regulatory environment gets materially worse in the U.S., not just Australia

• Snapchat+ subscriber growth stalls and the pivot to subscription revenue fails

• A competitor eats the core demographic (TikTok is the obvious name, but Instagram has been trying and failing at this for years)

None of those have happened yet. But I’m watching all of them. If the story changes, I’ll tell you in the Substack Notes

The Pick ’em Paul Bottom Line

I’m underwater. I know it. I’m not hiding it.

The TSI says $7.64. The stock is at $5.16. That’s a 48% implied upside if the model is in the right zip code. The bear case is real but not new. The Q4 numbers were mixed, not broken. And the product still works in my house every single day.

I’m selling covered calls, staying patient, and watching the next quarter like a hawk.

Pick ’em Paul Rule: Being underwater doesn’t mean being wrong. It means your thesis is being tested. Pass or fail, you’ll learn something either way.

This is JPM Picks. Just Paper Money, for entertainment and educational purposes only. Not financial advice. Not gambling advice. Do your own homework and never risk money you can’t afford to lose.

Have a $SNAP take? Considering a covered call or cash-secured put setup of your own? Hit reply. I’d love to hear how you’re thinking about it.