$ABT, a Love Story, and a Put I'm Watching Like a Hawk

Abbott Laboratories, a dividend king, a $91 strike, and what my aunt and uncle taught me about conviction.

My aunt and uncle met at Abbott Laboratories. He was in a testing role. She was in a testing role. Somewhere between the reagents and the results, they figured out they liked each other more than the job.

That was 29 years ago. My uncle still works there. Thirty-five years and counting.

I’ve always said, be careful who you talk to at work, you might end up married. My wife and I met at work too. Twenty-one years in, and she still puts up with me, most days.

So, when $ABT started showing up in my options screening, it was not a cold introduction. This is a company I’ve watched from a distance for a long time. Not just because of my family, but because Abbott is a Dividend King, a company that has raised its dividend for at least 50 consecutive years. Abbott has done it for 54 straight years. When a company has been writing bigger checks to shareholders longer than most people have been in the workforce, you pay attention to it.

I also spent years in the supplement industry, and Abbott acquired EAS back in 2004. EAS had a product called Betagen that I genuinely respected. That acquisition always stuck with me as a reminder that Abbott has a long history of buying quality and integrating it into something bigger. Whether that history applies to their latest big move is exactly what we are going to talk about.

Everything on JPM Picks is Just Paper Money, for entertainment and educational purposes only. Not financial advice, not gambling advice. Bet responsibly and never risk money you can’t afford to lose.

What Abbott Actually Is

Before we get into the trade and the mess, here is a quick frame on the company.

Abbott Laboratories is a diversified healthcare giant. They operate across four segments: medical devices (cardiovascular, diabetes management), diagnostics, nutrition (Ensure, Similac, they discontinued my beloved EAS in 2018), and established pharmaceuticals in international markets. About 60% of their sales come from outside the United States. Their market cap sits around $168 billion.

This is not a speculative name. This is a company that has been compounding for decades and has earned every bit of its blue-chip reputation.

Which makes what has happened to the stock in 2026 worth understanding.

The Trade

Abbott reported Q1 2026 earnings before the market opened on April 16th. Here is the short version of what happened.

EPS came in at $1.15, a penny better than Wall Street expected. Revenue came in at $11.37 billion, up nearly 7% year over year, but just shy of the consensus estimate of $11.40 billion. A $30 million miss on the top line is not normally a catastrophe, but the market did not stop there.

The real issue was guidance. Abbott cut its full-year adjusted EPS forecast from a range of $5.55-$5.80 down to $5.38-$5.58. That revision is almost entirely driven by the dilution impact from their $23 billion acquisition of Exact Sciences, the company behind the Cologuard colon cancer screening test. The deal closed earlier than expected, which is technically good news about the transaction itself, but it loaded debt onto the balance sheet sooner than Wall Street had modeled.

The stock had closed at $101.56 on April 15th. By the time the market closed on April 16th, it was down 6%.

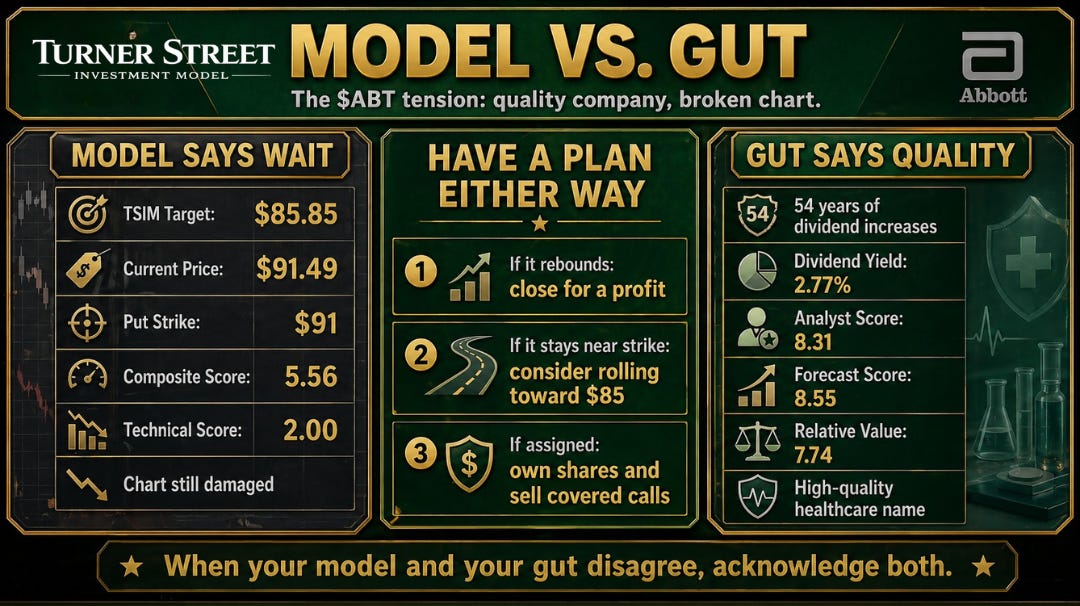

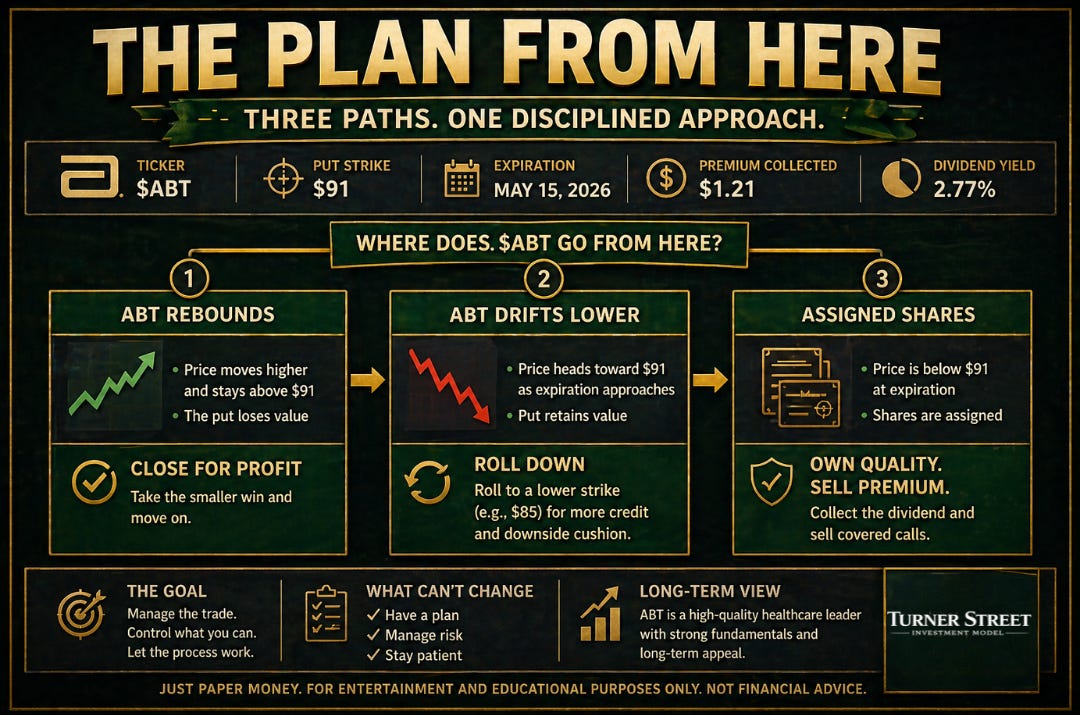

I saw a stock that had just beaten on earnings falling hard on a red day. My playbook says sell puts on red days because the premium tends to be richer when fear is up. So I sold the $91 put expiring May 15th for $1.21 in premium. The stock was around $96 when I pulled the trigger.

As of today, $ABT is sitting at $91.49. Nineteen days left.

I’m watching this one closely.

Why the Stock Is Actually Down

The earnings day drop was the most recent chapter, but the story started earlier. $ABT is down roughly 23% year to date and has pulled back more than 35% from its 52-week high near $136. That is not a one-day earnings reaction. That is a sustained re-rating.

Here is what is driving it:

The Exact Sciences acquisition is the biggest cloud. The $23 billion deal positions Abbott as a leader in oncology diagnostics, and CEO Robert Ford called it another high-growth addition to the portfolio. But acquisitions this size come with integration costs, added debt, and short-term EPS dilution. The market priced that in aggressively.

The nutrition segment is struggling. Q1 nutrition revenue fell 6% overall, with pediatric nutrition down 8.5%. Ensure and Similac are household names, but that part of the business is not growing right now.

NEC litigation is a real risk. An Illinois jury awarded $70 million in damages to families who alleged that Abbott’s Similac Special Care 24 formula caused necrotizing enterocolitis in premature infants. Abbott is appealing, and the judgment came through an established legal process rather than out of nowhere, but more cases are pending. That kind of overhang weighs on any stock, especially a name that has built its reputation on reliability.

Tariffs are adding noise. Abbott committed $500 million to expand U.S. manufacturing in Illinois and Texas to reduce exposure over time, but the near-term cost headwinds are expected to persist through at least the first half of this year.

And on April 22nd, Daiwa downgraded $ABT from Outperform to Neutral, citing near-term headwinds in the medical devices segment. The stock dropped another 1.1% that day and pushed toward its 52-week low of $91.59. That is a real wall of worry. I am not going to pretend it is not.

What the TSIM Says (And Where It Gets Interesting)

I ran Abbott through the Turner Street Investment Model, and this is where it gets honest and a little uncomfortable at the same time.

The TSIM produces a JPM Picks target price of $85.85. The stock is currently at $91.49. That means, by my own model, I sold a put at a strike price that my framework says might not even represent fair value yet.

I will own that. That is the position I am in.

But here is what makes this more interesting than just a bad trade thesis. Look at how the six pillars actually scored:

Fundamentals: 6.61 | Analyst: 8.31 | Technical: 2.00 | Market Implied: 6.18 | Relative Value: 7.74 | Forecast: 8.55

Composite Score: 5.56

Five of the six pillars are telling a constructive story. The Analyst score at 8.31 reflects a consensus target near $120 across 28 analysts, most of whom maintain Buy or Strong Buy ratings. The Forecast score at 8.55 says the probability-weighted scenario analysis likes the stock’s forward setup. The Relative Value score at 7.74 says Abbott looks cheap relative to its peers right now.

And then there is the Technical score.

A 2 out of 10.

The chart on $ABT is broken. The stock is trading well below its 200-day moving average, which sits near $122. The RSI hit 25 last week, putting it in the extremely oversold category. An RSI of 25 does not automatically mean buy, but it does mean the selling has been aggressive and sustained. It also means the technical picture alone is enough to drag a composite score down hard.

The model composite lands at 5.56, right in the Hold or Watch zone. The model is not screaming buy. It is also not screaming sell. It is saying: the fundamentals and the analyst community see real value here, the chart is a wreck, and the truth probably lives somewhere in between. That is the tension this trade is sitting inside.

The Bull Case

Here is where I land after all of it.

Abbott is a franchise. Fifty-four consecutive years of dividend increases does not happen by accident. You do not build that record without a real underlying business and real management discipline. My uncle has given 35 years of his career to this company. That is not the kind of institution that collapses because of one rough acquisition cycle.

The Exact Sciences deal is a long-term bet on oncology diagnostics, one of the fastest-growing areas in healthcare. Cologuard has real market penetration and genuine upside. The market is valuing that upside at distressed prices right now because of short-term EPS dilution. That trade often looks wrong before it looks right.

The analyst community at 8.31 knows more than I do. I am going to say that out loud because it is true. When 28 analysts covering the same company are pointing to a consensus target around $120 and the stock is trading at $91, the gap is worth acknowledging. Analysts have been wrong before, but that kind of alignment is not nothing.

Is this a flawless setup? No. Is this a quality company going through a difficult stretch that the market is pricing like something more permanent? That is the case I am making.

The Plan Going Forward

Here is exactly where I am on the $91 put with 19 days left.

If the stock moves back into positive territory on my position, I close it for a smaller profit and move on. Premium in the pocket, lesson learned about strike selection relative to what my own model was saying, next trade.

If I cannot close it for a gain and we are sitting at or near the strike close to expiration, I will look to roll the position down toward the $85 level and try to collect a net premium credit in the process. That gets my effective exposure closer to what the TSIM actually says is fair value territory.

And if neither of those works out and I end up assigned at $91, I am genuinely okay owning this stock. If this position turns into share ownership, I sell covered calls along the way to grind down the cost basis. That is the JPM Picks way. The wheel does not stop just because the first spin went sideways.

The JPM Take

I am in a put I probably should not have entered at that strike according to my own model, that is the honest version. The TSIM said $85.85 and I sold a $91 put. The model is still in the testing phase, which is exactly why it is called V3 and not the final word.

But I am not convinced the model is telling me to panic either. Five of six pillars see real value here. The Analyst and Forecast scores, two of the most forward-looking pillars in the framework, both land in the 8s. What is broken is the chart, and charts do not stay broken forever on companies with 54 years of consecutive dividend increases and a management team still buying back shares at these levels.

Quality companies go on sale sometimes. Abbott is on sale.

Whether the sale is over or has more to go is the honest question I cannot answer with certainty. What I can give you is the plan, the position, and where the data actually points. The rest is process.

I will update you when this one resolves, one way or another. (Follow me on X for updates)

Pick ‘em Paul Rule: When your model and your gut disagree, acknowledge both, have a plan for either outcome, and never pretend you knew all along.

This is JPM Picks. Just Paper Money, for entertainment and educational purposes only. Not financial advice. Not gambling advice. Do your own homework and never risk money you cannot afford to lose.

Watching $ABT closely and thinking about your own put or covered call setup? Hit reply. I want to hear how you are thinking about it.