Two Premiums, One Direction: The Covered Strangle

How to collect premium from both sides of a trade without a margin account.

As I got further into options trading, I started wondering whether there was a way to collect extra premium without taking on a ton of extra risk.

It turns out there is. But it comes with conditions. And it only works if you already understand the basics of how covered calls and cash-secured puts function. If you are still fuzzy on those, the Options 101 post is the place to start.

If you are comfortable with the wheel strategy and you want to look at a variation that can accelerate cost basis reduction in a flat market, keep reading.

What I want to roll through today is the covered strangle.

What Is a Covered Strangle?

Let me build it piece by piece.

You already know what a covered call is. You own 100 shares, you sell a call above the current price, and you collect premium in exchange for agreeing to sell your shares at the strike if the stock runs up past it.

You already know what a cash-secured put is. You set cash aside in your account, you sell a put below the current price, and you collect premium in exchange for agreeing to buy 100 shares at the strike if the stock drops below it.

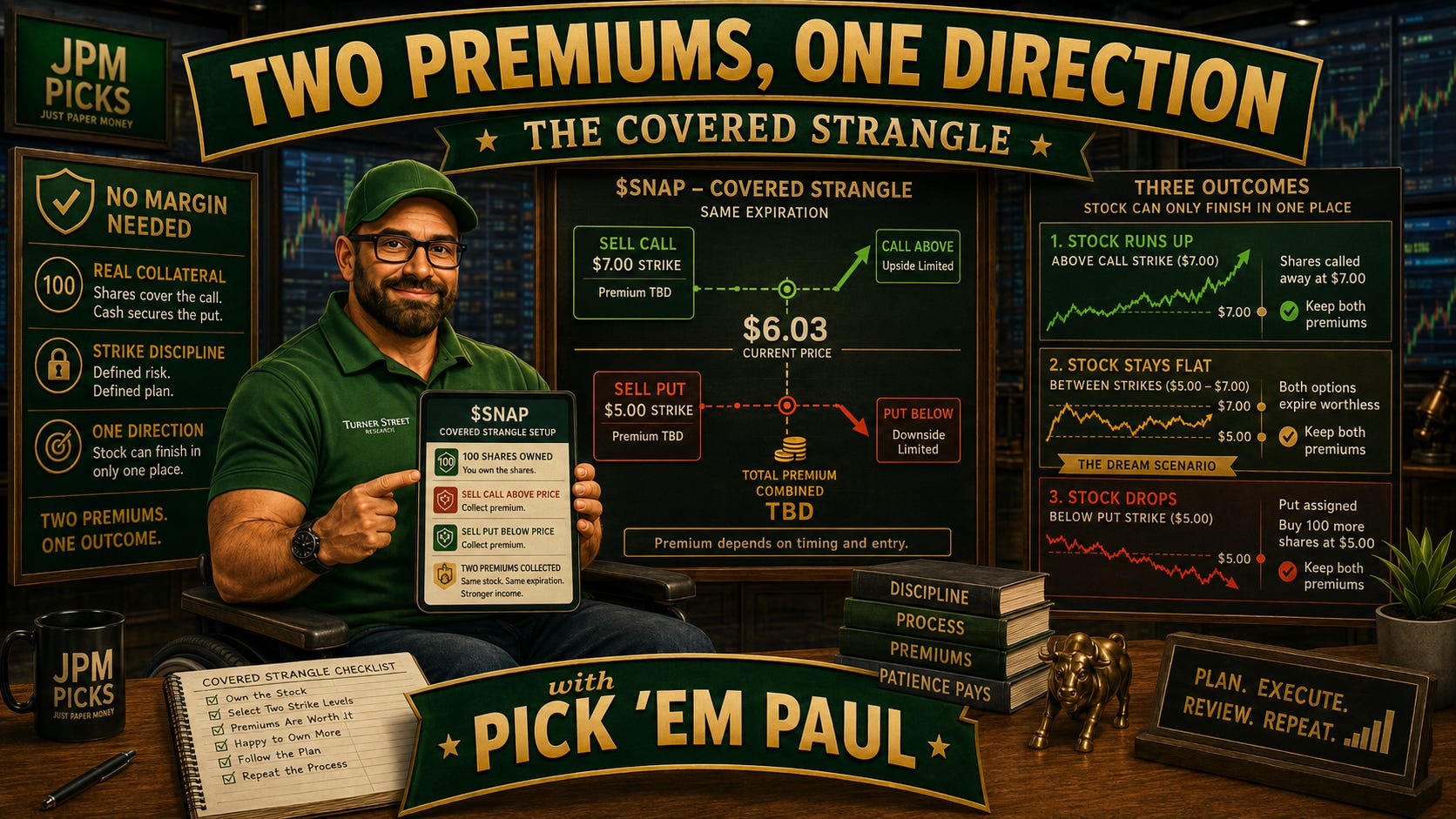

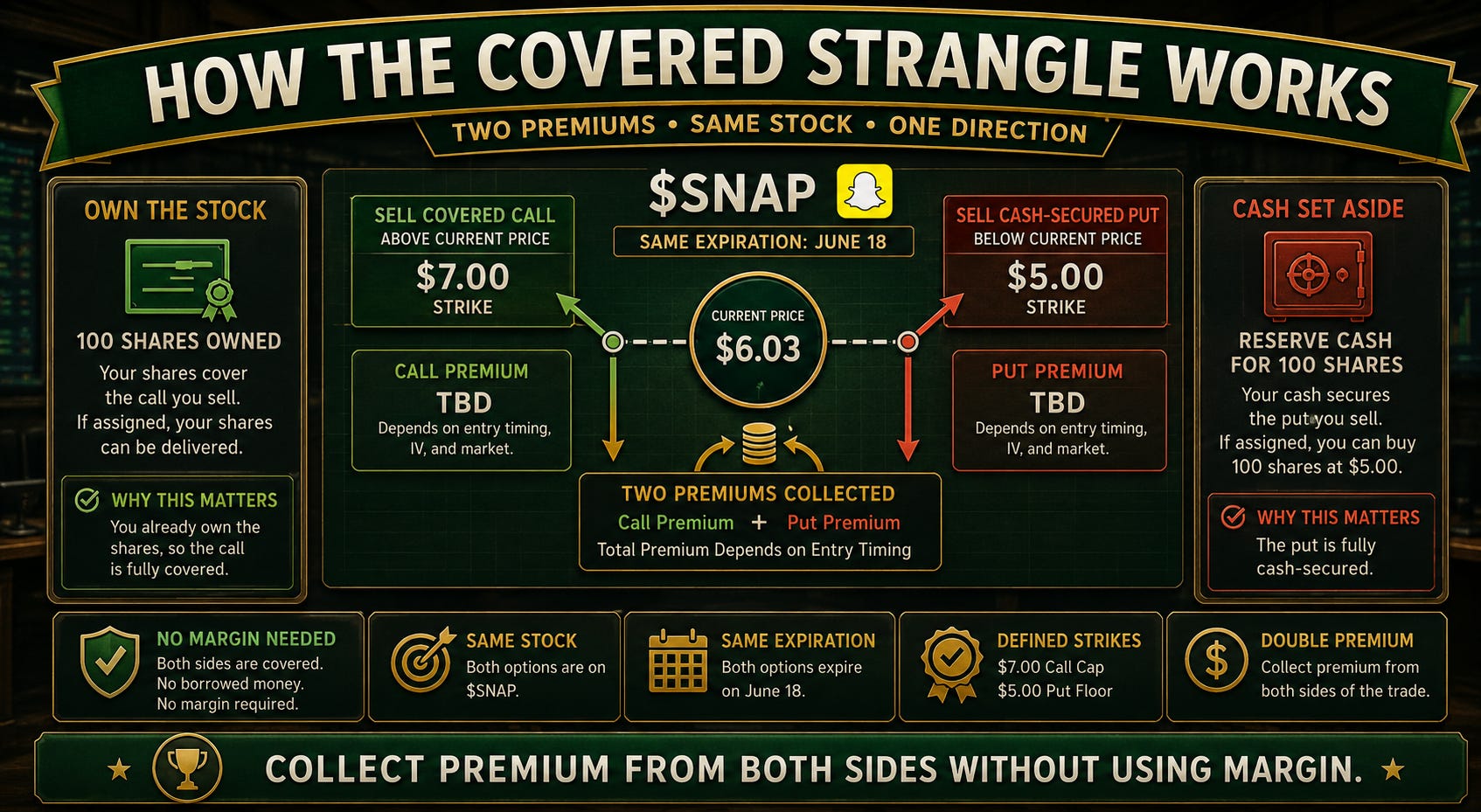

A covered strangle is just both of those happening at the same time.

• You own 100 shares

• You sell an out-of-the-money call above the current price (covered by your shares)

• You sell an out-of-the-money put below the current price (cash-secured by money sitting in your account)

Two contracts open at once. Two premiums collected on the same trade. Same stock. Same expiration date.

I really like this strategy because it does not require a margin account, at least in my experience with Robinhood and Schwab. I refuse to use margin accounts because they tend to push investors and traders toward taking on more risk than they are actually comfortable with. The leverage feels free until it is not, and I have seen too many people blow up a good process by borrowing their way into a bad position. That is not what JPM Picks is about.

The reason no margin is needed comes down to how the two sides of the trade are collateralized. The call is covered because you own the shares. The put is cash-secured because you have the money sitting in your account to back it. No borrowed capital. No brokerage leverage. Just real collateral on both sides.

The Part That Makes This Work: One Direction

Here is the core insight that makes the covered strangle more interesting than it sounds at first.

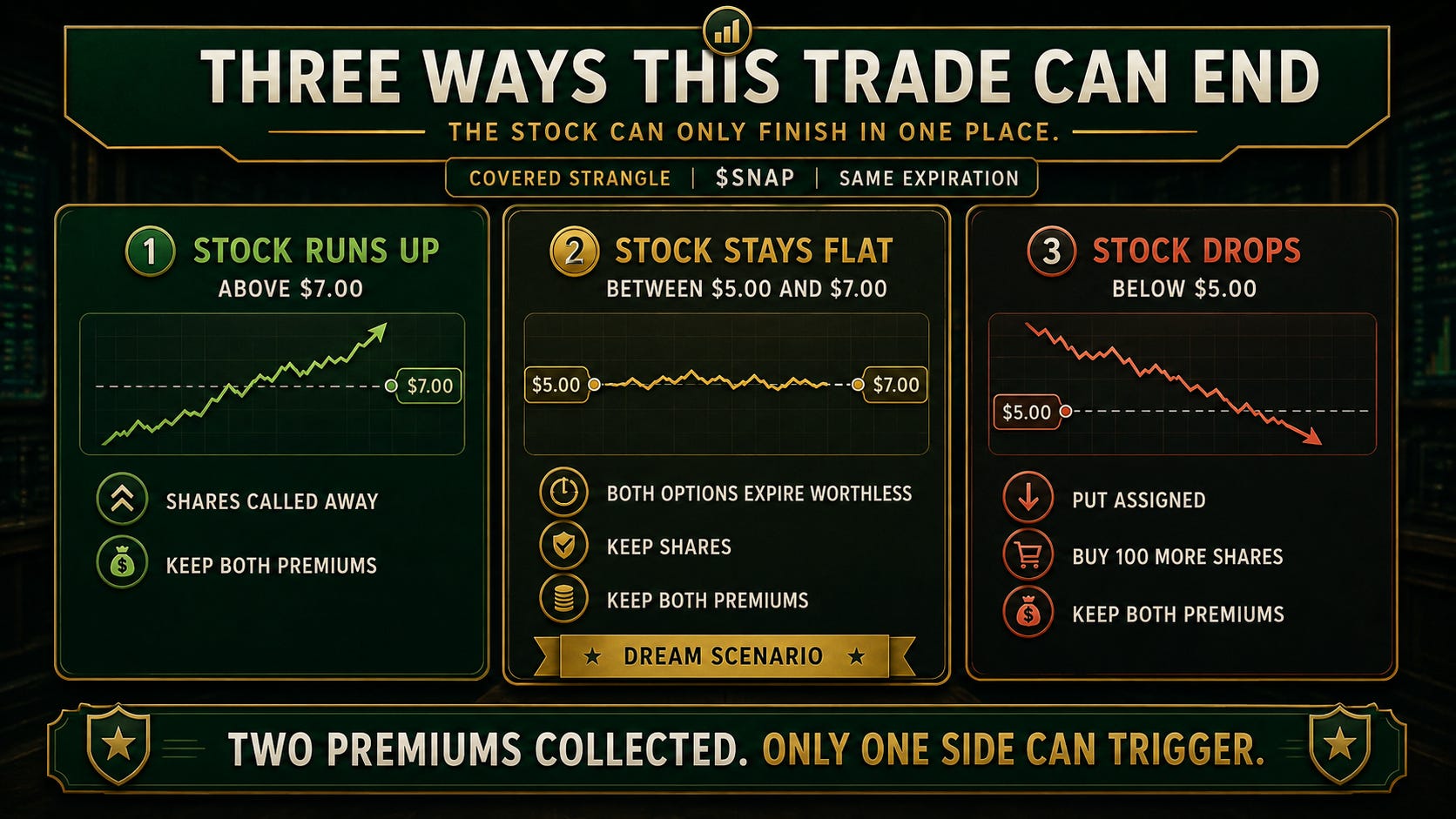

A stock can only finish in one place at expiration.

Your put strike is below the current price. Your call strike is above it. The stock will either close above the call strike, below the put strike, or somewhere in between. It cannot be in two places at once. Which means you cannot be assigned on both sides simultaneously.

Let that land for a second. You collected premium from two contracts, but only one of them can ever be assigned.

That is the key. The covered strangle is not a way to take on double the risk. It is a way to collect double the premium while only one side can ever turn into an obligation at expiration.

The Three Outcomes

What actually happens depending on where the stock closes.

Outcome One: The Stock Runs Up Past the Call Strike

Your shares get called away at the call strike. You collect the sale proceeds plus the call premium. The put expires worthless, and you keep that premium too.

You are no longer in the trade. You have cash, two rounds of premium, and a clean exit. Not a bad result.

Outcome Two: The Stock Stays Flat (The Dream Scenario)

This is the one that makes the covered strangle genuinely exciting.

Both options expire worthless. You keep your 100 shares. You keep the call premium. You keep the put premium. No assignment on either side.

In a flat or slow-moving market, that double premium hits your cost basis from both directions at once. If your shares cost you $50 each and you collected $0.60 in call premium and $0.80 in put premium, your effective cost basis just dropped from $50 to $48.60 in one expiration cycle. Run that a few times and you start to see why this strategy is interesting for people who want to hold a position long-term.

Outcome Three: The Stock Drops Below the Put Strike

The put gets assigned. You buy 100 more shares at the put strike. The call expires worthless.

You still keep both premiums, which softens the effective entry price on the new shares. But now you own 200 shares of a stock that is trading lower. That is the real risk here, and you should not look past it casually.

This is why the covered strangle only makes sense on stocks you would genuinely be comfortable adding to. Not stocks you are already nervous about. Not stocks where you would panic at 200 shares if the price kept dipping.

Why I Like It (And When I Use It)

The wheel strategy is my foundation. Cash-secured puts to enter, covered calls once I own shares, repeat.

The covered strangle is a variation I layer in when a few conditions line up. The stock needs to be one I already own and believe in. The premiums on both sides need to make sense for the strikes I am comfortable with. And I need to be honest with myself about whether I would be okay with owning more shares if the put gets triggered.

The flat market scenario is where this really shines. In a sideways environment where stocks are not moving much, a standard covered call collects one round of premium. The covered strangle collects two. For a position I plan to hold long-term regardless, doubling the premium income in a quiet week is not a small thing. It adds up, especially over multiple cycles.

The reason I can do this without a margin account is worth repeating. The call is covered by shares I already own. The put is backed by cash I have set aside. Both sides have real collateral. That is fundamentally different from a spread strategy, which uses one option to partially offset the risk of another and typically requires margin approval from your broker.

If your brokerage does not allow spreads, the covered strangle may still be available to you if you have the shares and the cash. Worth checking.

A Live Example: What This Looks Like in Practice

I do not want to just explain this in the abstract, so here is what I am actually looking at this week.

If you were reading JPM Picks back in February, you might remember the post titled I’m Underwater on $SNAP and I’m Still Bullish. That was one of the most-read posts on this Substack, and the short version was this: I owned shares, I was underwater, I still believed in the stock, and my plan was to sell covered calls to grind down my cost basis while I waited.

That plan has been working. As of this writing, $SNAP is sitting at $6.03, and my cost basis is right at $6. I am no longer underwater. I am just barely above water, which feels a lot better than where this thing started.

Now, with earnings recently reported and no major catalysts expected in the next 30 days, I am looking at the next evolution of this trade: the covered strangle. An earnings event can blow through your strikes in a hurry, so I want the calendar clear before I set up both legs.

Here is the plan for building the covered strangle in two legs.

Leg One, the covered call: If $SNAP opens green on Monday, I will sell a covered call at either the $6.50 or $7.00 strike expiring June 18th. Which strike I pick will depend on where the stock opens and what the premium looks like at that moment. Both are above my cost basis, so either is a price I would be okay selling at.

Leg Two, the cash-secured put: If $SNAP opens red on Monday, I will sell the $5 cash-secured put expiring June 18th instead and look for a green day later in the week to add the covered call. If the stock opens green and I sell the call first, I will look for a red day during the week to complete the put leg.

The point is that I am staging both entries based on what the market gives me. A green open means richer call premium. A red open means richer put premium. I want both legs entered into favorable conditions, not both placed at the same time just because the timing is convenient.

If the stock stays flat through June 18th and both options expire worthless, I collect premium from both sides, keep my shares, and my cost basis drops further below $6. That is the scenario I am rooting for. And if one side gets assigned, I have already decided I am okay with either outcome: selling my shares at $6.50 or $7 or buying more at $5.

I will follow up on this trade in a future post once the positions are fully set.

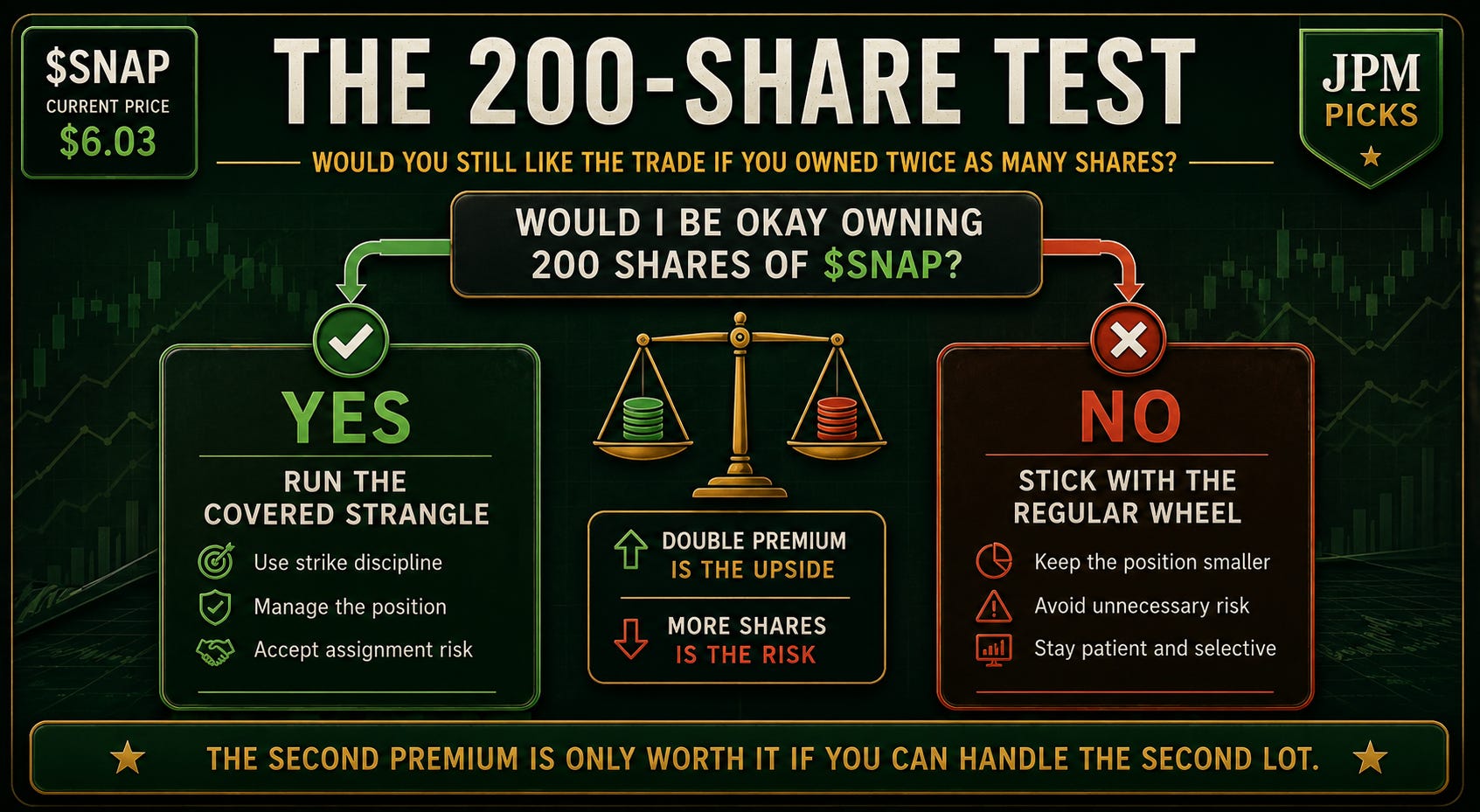

The One Rule That Keeps It Honest

Before you run a covered strangle, answer this question.

Would I be okay owning 200 shares of this stock if things went sideways?

Not a rhetorical question. A real one.

If the answer is yes, the covered strangle is worth considering. If the answer is anything else, the regular wheel is the right move. The second lot of premium is only worth having if you are genuinely prepared for what it costs when the put gets assigned.

The strategy works best when you combine it with strike discipline. Do not sell the put at a strike you would not have sold anyway. Do not sell the call at a strike you would not have sold anyway. If both positions hold up on their own, the combination should too.

The Pick ‘em Paul Bottom Line

The covered strangle is not a magic trick. It is a logical extension of strategies you already understand.

You own shares. You sell a call. You also sell a put. You collect premium from both. The stock only closes in one place, so only one side can trigger. If the stock stays flat, you collect both and hold your position. If you get assigned on the put, you were already okay owning more.

It accelerates cost basis reduction in slow markets. It does not require margin. And it fits naturally inside the wheel framework for anyone who is already comfortable with covered calls and cash-secured puts.

Like every options strategy, it is not for everyone, and it is not for every stock. But if you have been running the wheel for a while and you are looking for a logical next step, the covered strangle is worth understanding.

Pick ‘em Paul Rule: The covered strangle rewards patience and flat markets. The double premium is the upside. Owning more shares of a falling stock is the risk. Know which one you are prepared for before you place the trade.

This is JPM Picks. Just Paper Money, for entertainment and educational purposes only. Not financial advice. Not gambling advice. Always do your own homework and never risk money you cannot afford to lose.

Are you running covered calls or cash-secured puts already? Have you ever tried combining them at the same time? Hit reply and let me know what your experience has been.